Unpacking the EU’s Latest Directive on Sustainability Reporting

The Directive 2013/34/EU of the European Parliament and of the Council, is a part of the Green Deal initiative from the European Union to direct economic growth from resource use to a socially sustainable economic system.

This directive establishes a comprehensive sustainability reporting framework for companies listed in the European Union to provide more consistent, comparable, and reliable information to investors and other stakeholders, with some key takeaways as below.

Key Takeaways

- Company Categories Affected: Large public-interest companies with more than 500 employees are required to disclose non-financial and diversity information from January 1st, 2024; other large companies by 2025, and Small and Medium Enterprises (SMEs) by 2026.

- Key Areas of Reporting: Organizations were to report on environmental, social, and employee-related matters, respect for human rights, anti-corruption, and bribery issues.

- Integration with Business Strategy: Companies are required to disclose information about how ESG matters are pursued in their business model; policies, including due diligence processes implemented; the outcome of those policies; risks and risk management; and key performance indicators relevant to the business.

- Integration with Financial Reporting: The non-financial statement should be included in the management report and needs to be related to the company’s development, performance, position, and the impact of its activities.

- Reporting Format: Sustainability reporting should be published in a digital format.

- Methodology Flexibility: While companies were given significant flexibility in how they report (e.g., they could use international, European, or national guidelines), they were to provide a clear and non-misleading view of their development, performance, position, and the impact of their activity.

- Targeted Stakeholders: The first group of users consists of investors, including asset managers, who want to better understand the risks and opportunities that sustainability issues pose for their investments and the impacts of those investments on people and the environment.

The second group of users consists of civil society actors, including non-governmental organizations and social partners, which wish to better hold undertakings to account for their impacts on people and the environment.

Other stakeholders might also make use of sustainability information disclosed in annual reports, in particular, to foster comparability across and within market sectors.

- Due Diligence and Accountability: There was an emphasis on due diligence processes to identify, prevent, mitigate, and account for human rights abuses and environmental issues in their own operations and their value chains.

- Assurance Providers: Statutory auditors or audit firms should provide limited assurance on sustainability reporting, evolving to reasonable assurance over time.

Member states can also allow accredited independent assurance services providers.

- Expands Scope: Also applicable to companies like credit institutions, insurance companies, and large subsidiaries of non-EU companies operating in the EU.

- Tax Reporting: Companies should start reporting on how and to what extent their activities meet the criteria set out in the taxonomy, which incentivizes green investments.

For over a decade, the European Union (EU) has made significant steps in advancing sustainability-related disclosures.

Beginning with the Non-Financial Reporting Directive (NFRD) in 2013, the EU has now introduced the Sustainability Reporting Standards in mid-2023 and is expected to roll out to all businesses listed on the EU market by 2026.

Below is a key timeline for compliance.

Key Timeline for Compliance:

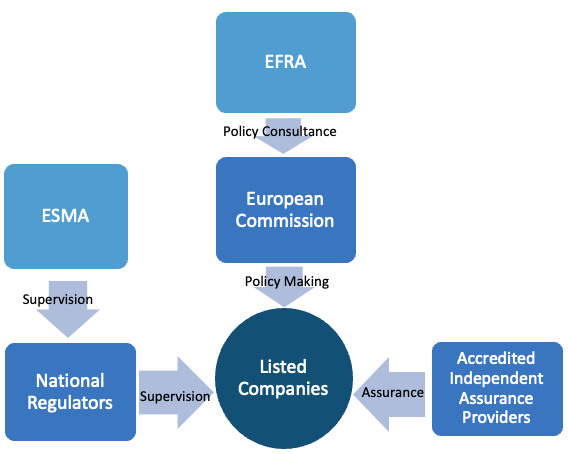

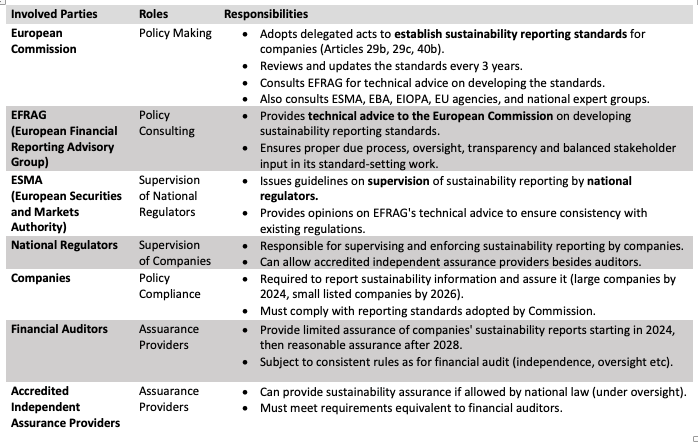

In addition to policymakers and impacted businesses, the roles and responsibilities of supervisory and assurance entities are detailed below.

The Roles and Responsibilities of Diverse Parties

This new EU directive underscores a continuous effort to enhance sustainability disclosure requirements, aligning closely with the European Green Deal and the sustainable finance strategy.

In fact, some of these changes would have happened in any case, spurred by rapidly shifting citizen awareness, consumer preferences, and market practices.

The COVID-19 pandemic has further emphasized this urgency, highlighting vulnerabilities in workers and business value chains.

Therefore, there is a clear need for a robust and affordable reporting framework.

This framework must be paired with effective auditing practices to ensure the reliability of data and prevent issues such as greenwashing and double counting.

As the legislation strives to match the evolving market needs for ESG information, we can expect the requirements and focus areas will continue to adapt in the coming years.

Ready to make your business more sustainable and gain a competitive edge?

At Taze Consulting, we specialize in financial transformation for businesses.

Contact us for a no-obligation chat about your needs.

References: